It is a topic that no one likes to think about, but the importance of making a proper Will cannot be emphasised enough.

If a person dies without leaving a Will this is known as dying “intestate”. This can also happen if a person has a will, but the Will is invalid because, for example they did not have proper mental capacity or if the formal requirements for a valid will have not been met.

The implications of dying intestate

If a person dies intestate, the law determines how the estate will be divided after the payment of all their debts. The rules for intestate succession are anything but simple and can vary depending on both the size of the estate and the number and class of relatives remaining after a person’s death. In addition to that, working out how the rules apply, and who is entitled to be the Administrator (see below) is often a very time-consuming process and can lead to unnecessary disputes over the estate and large extra costs. This can lead to a huge amount of frustration for the surviving family members involved in the administration of the estate.

Normally a person will nominate an executor who will deal with the estate in their will. If there is no will, a family member of the deceased must make an application to the Probate Office of the Supreme Court for permission to administer the estate. The person making the application must be over 18 and entitled to a share of the inheritance. The appointed person is known as the administrator of the estate. If no one takes this responsibility, the Public Trustee will administer the estate. The process for being appointed, and the duties of the Administrator, can be confusing and often require the assistance of a lawyer.

If you want to read more on when you should consider planning your will, read our comprehensive blog!

Who will inherit if a person dies intestate

The first in line to inherit will be the spouse and then the children of the deceased, or a combination of the two depending on the size of the estate. A de facto partner can also inherit in the same way a spouse does if the de facto partnership can be proven. Not leaving a will places an unnecessary burden on the surviving de facto partner to prove the existence of the relationship, something that could easily be avoided by nominating the person as a beneficiary in a will instead.

If a person is married and has no children, a share of the estate can also go to the deceased’s parents, depending on the value of the estate, which may be contrary to the wishes of the deceased if they intended for their spouse/partner to inherit the whole of their estate.

If a person is married and has no children, a share of the estate can also go to the deceased’s parents, depending on the value of the estate, which may be contrary to the wishes of the deceased if they intended for their spouse/partner to inherit the whole of their estate.

If a person does not have a spouse/partner or children, other family members like parents, siblings and aunts and uncles will be next in line to inherit the estate. This can also be contrary to the wishes of a person if they were estranged from their family during their lifetime.

If no relatives can be found, the estate will be claimed by the State.

What happens if the deceased has minor children

A significant problem can arise if a person has minor children and no guardian has been appointed in a will. If this happens, a court must appoint a guardian. This often leads to disputes over guardianship and a large amount of unnecessary legal fees being incurred.

Under intestacy law, if a person dies leaving minor children, the children will inherit their share of the estate when they become 18. At the age of 18, people are often not experienced enough to make sensible decisions on how best to deal with an inheritance. If a will is made, a trust can be created, or a provision can be made that the children would only inherit their share at a later age.

Your will does not necessarily cover your super or life insurance

A superannuation death benefit is the amount left in your super fund account after you die. This will not automatically form part of a person’s estate and will ordinarily be paid to the person who is nominated under a death benefit nomination. Provisions can be made in a will that a death benefit forms part of your estate.

This is, itself, not binding on the trustee of your superannuation fund, however. If you want your superannuation to be left under your will then you must also give your superannuation fund trustee a binding death benefit nomination which states that on your death your superannuation death benefits should be paid to the executor of your estate. If your death benefit nomination is non-binding, however, the Trustee of the Superannuation Fund can decide whether to comply with it or whether to distribute the death benefit to other close relatives specified in the superannuation law.

The same applies to life insurance that is held outside a superannuation fund: the benefit of the policy will not form part of your estate if you have nominated a beneficiary to receive your life insurance on your death. If you want your life insurance to be paid to the executor and dealt with as if it forms part of your estate, then you should either not nominate a beneficiary or nominate “the executor of my estate to be dealt with in accordance with the terms of my will” as the beneficiary of the policy. In that case your will should also contain a clause stating that if your executor receives any proceeds from a life insurance policy they must deal with that in the same way as your estate.

If you don’t have a will then the risks of your superannuation and life insurance policy proceeds ending up in the wrong hands are considerably increased.

Property is owned together with others after you die

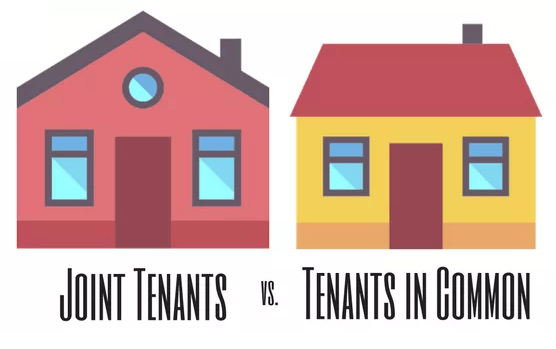

If a person owns a property together with another person as “tenants in common”, their share in the property will be administered in terms of intestacy law if they do not leave a will, whereas if the person had a will they can decide what happens with their share of the property when they die.

If a person owns a property together with another person as “tenants in common”, their share in the property will be administered in terms of intestacy law if they do not leave a will, whereas if the person had a will they can decide what happens with their share of the property when they die.

If they own a property together with another person as “joint tenants” their share will automatically pass to the surviving owner, as their share of the property does not form part of their estate. In this case it does not matter whether the person made a will or not. A person who owns a share of a property as a “joint tenant” who does not want their share to go to the other owner when they die should take legal advice about strategies to avoid this occurring. Read more about capital gains tax here.

The law of succession can be complicated and by consulting with an expert estate planning lawyer you will have peace of mind that all the formalities have been met and that your wishes have been correctly recorded.

If you would like to have a will prepared or have a discussion on estate planning, please get in touch with us on ka*************@*****************om.au or st*****@*****************om.au